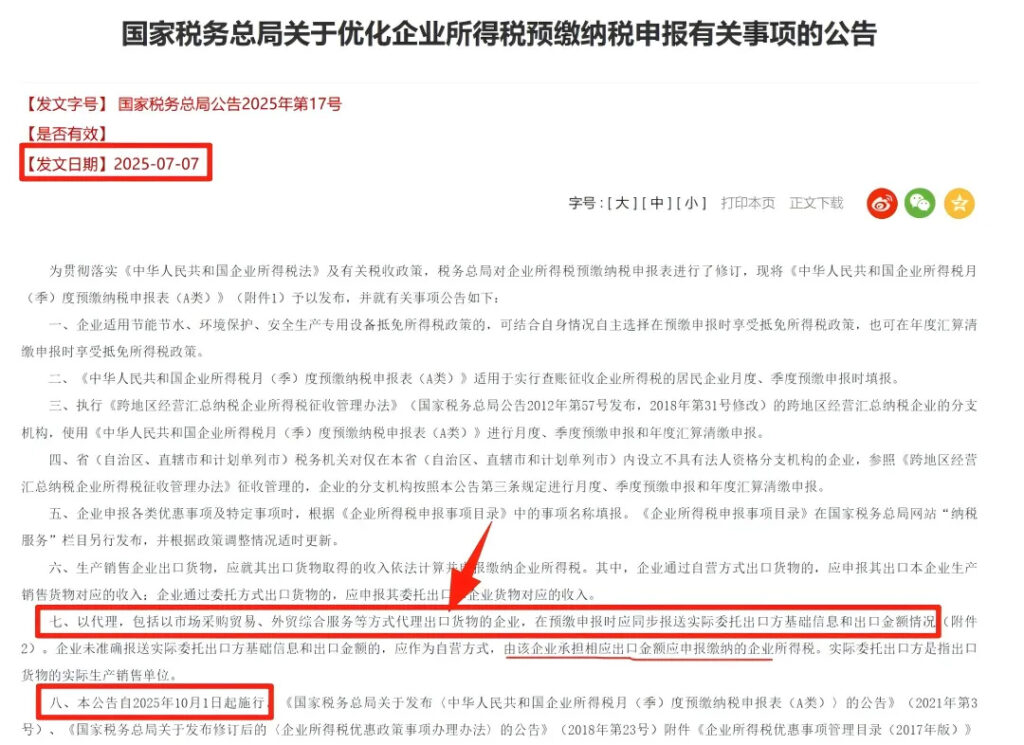

Recently, a document from the State Taxation Administration has gone viral in the cross-border community! Announcement No. 17 of 2025 will take effect on October 1.

Additionally, e-commerce exports involve a wide variety of goods. Under the previous “purchase order” export method, declarations typically used simplified product names for high-volume items. With the new regulations in place, information such as product names, HS codes, and goods value must strictly reflect actual circumstances. This means that tasks like preparing customs declarations and data entry will significantly increase, while the time required for document preparation and review will also lengthen.

How should one respond? For cross-border e-commerce enterprises at different stages of development, we have compiled the following solutions for reference:

1. Verkäufer, die Steuerrückerstattungszollanmeldungen ausgefüllt haben

Continue to export, receive foreign exchange, and claim tax rebates under your company's name without any impact. Proceed as usual. In the long term, you can also maintain the benefits of export tax rebates.

2. Growth-oriented sellers (with stable business operations)

Consider applying for import-export rights to pursue a self-operated export model. This allows you to declare exports under your own company name and independently handle customs clearance, foreign exchange receipts, and tax filings. While the initial procedures and investment are substantial, this approach enhances corporate creditworthiness in the long run and is more conducive to profit growth and compliant operations.

3. Startup sellers (without export qualifications)

Exporting through an agent is permissible, but must be conducted in compliance with regulations:

Sellers must engage licensed agents (with registered import/export credentials) or reputable customs brokerage firms to execute agency agreements for export processing. Sellers shall provide transaction documentation including “manufacturer/seller details + packing list + pro forma invoice” and pay reasonable agency fees.

The key point is: To ensure accurate reporting, you must provide genuine information about the exported goods, particularly their value. At the same time, minimize frequent changes in the consignee company to avoid data discrepancies that could lead to unnecessary tax risks.